Weekly Tax Brief

How IRS auditors learn about your business industry

- Details

- Published: 10 October 2023 10 October 2023

Ever wonder how IRS examiners know about different industries so they can audit various businesses? They generally do research about specific industries and issues on tax returns by using IRS Audit Techniques Guides (ATGs). A little-known fact is that these guides are available to the public on the IRS website. In other words, your business can use the same guides to gain insight into what the IRS is looking for in terms of compliance with tax laws and regulations.

Many ATGs target specific industries, such as construction, aerospace, art galleries, architecture and veterinary medicine. Other guides address issues that frequently arise in audits, such as executive compensation, passive activity losses and capitalization of tangible property.

Issues unique to certain taxpayers

IRS auditors need to examine all different types of businesses, as well as individual taxpayers and tax-exempt organizations. Each type of return might have unique industry issues, business practices and terminology. Before meeting with taxpayers and their advisors, auditors do their homework to understand various industries or issues, the accounting methods commonly used, how income is received, and areas where taxpayers might not be in compliance.

By using a specific ATG, an IRS auditor may be able to reconcile discrepancies when reported income or expenses aren’t consistent with what’s normal for the industry or to identify anomalies within the geographic area in which the business is located.

Updates and revisions

Some guides were written several years ago and others are relatively new. There isn’t a guide for every industry. Here are some of the guide titles that have been revised or added in recent years:

- Entertainment Audit Technique Guide (March 2023), which covers income and expenses for performers, producers, directors, technicians and others in the film and recording industries, as well as in live performances;

- Capitalization of Tangible Property Audit Technique Guide (September 2022), which addresses potential tax issues involved in capital expenditures and dispositions of property.

- Oil and Gas Audit Technique Guide (February 2023), which explains the complex tax issues involved in the exploration, development and production of crude oil and natural gas;

- Cost Segregation Audit Technique Guide (June 2022), which provides IRS examiners with an understanding of why and how cost segregation studies are performed in order for businesses to claim refunds related to depreciation deductions.

- Attorneys Audit Technique Guide (January 2022), which covers issues including retainers, contingent fees, client trust accounts, travel expenses and more;

- Child Care Provider Audit Technique Guide (January 2022), which enables IRS examiners to audit businesses that provide care in homes or day care centers; and

- Retail Audit Technique Guide (March 2021), which details tax issues unique to businesses that purchase items from a supplier or wholesaler and resell them at a profit.

Although ATGs were created to help IRS examiners uncover common methods of hiding income and inflating deductions, they also can help businesses ensure they aren’t engaging in practices that could raise audit red flags. For a complete list of ATGs, visit the IRS website.

© 2023

Casualty loss tax deductions may help disaster victims in certain cases

- Details

- Published: 06 October 2023 06 October 2023

This year, many Americans have been victimized by wildfires, severe storms, flooding, tornadoes and other disasters. No matter where you live, unexpected disasters may cause damage to your home or personal property. Before the Tax Cuts and Jobs Act (TCJA), eligible casualty loss victims could claim a deduction on their tax returns. But currently, there are restrictions that make these deductions harder to take.

What’s considered a casualty for tax purposes? It’s a sudden, unexpected or unusual event, such as a hurricane, tornado, flood, earthquake, fire, act of vandalism or a terrorist attack.

Many unable to claim a tax break

For losses incurred from 2018 through 2025, the TCJA generally eliminates deductions for personal casualty losses, except for losses due to federally declared disasters.

Note: There’s an exception to the general rule of allowing casualty loss deductions only in federally declared disaster areas. If you have personal casualty gains because your insurance proceeds exceed the tax basis of the damaged or destroyed property, you can deduct personal casualty losses that aren’t due to a federally declared disaster up to the amount of your personal casualty gains.

Claim a refund with a special election

If your casualty loss is due to a federally declared disaster, a special election allows you to deduct the loss on your tax return for the preceding year and claim a refund. If you’ve already filed your return for the preceding year, you can file an amended return to make the election and claim the deduction in the earlier year. This can potentially help you get extra cash when you need it.

This election must be made no later than six months after the due date (without considering extensions) for filing your tax return for the year in which the disaster occurs. However, the election itself must be made on an original or amended return for the preceding year.

Calculating the deduction

You must take the following three steps to calculate the casualty loss deduction for personal-use property in an area declared a federal disaster:

- Subtract any insurance proceeds.

- Subtract $100 per casualty event.

- Combine the results from the first two steps and then subtract 10% of your adjusted gross income (AGI) for the year you claim the loss deduction.

Important: Another factor that makes it harder to claim a casualty loss than it was years ago is that you must itemize deductions to claim one. Through 2025, fewer people will itemize because the TCJA significantly increased the standard deduction amounts. For 2023, they’re $13,850 for single filers, $20,800 for heads of households, and $27,700 for married joint-filing couples. So even if you qualify for a casualty deduction, you might not get any tax benefit because you don’t have enough itemized deductions.

Lawmakers debate the issue

Earlier this year, a bipartisan group of lawmakers in Washington introduced a bill that would make the deduction available to more taxpayers. The proposed Casualty Loss Deduction Restoration Act would reinstate the deduction to all taxpayers with a casualty loss — not just those located in a federal disaster declaration area. Passage of the bill is uncertain at this time.

We can help

The rules described above are for personal property. Keep in mind that the rules for business or income-producing property are different and other rules may apply. (It’s easier to get a deduction for a business property casualty loss.) If you’re a victim of a disaster, we can help you understand the complex tax deduction rules.

© 2023

What types of expenses can’t be written off by your business?

- Details

- Published: 04 October 2023 04 October 2023

If you read the Internal Revenue Code (and you probably don’t want to!), you may be surprised to find that most business deductions aren’t specifically listed. For example, the tax law doesn’t explicitly state that you can deduct office supplies and certain other expenses. Some expenses are detailed in the tax code, but the general rule is contained in the first sentence of Section 162, which states you can write off “all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business.”

Basic definitions

In general, an expense is ordinary if it’s considered common or customary in the particular trade or business. For example, insurance premiums to protect a store would be an ordinary business expense in the retail industry.

A necessary expense is defined as one that’s helpful or appropriate. For example, let’s say a car dealership purchases an automated external defibrillator. It may not be necessary for the operation of the business, but it might be helpful and appropriate if an employee or customer suffers cardiac arrest.

It’s possible for an ordinary expense to be unnecessary — but, in order to be deductible, an expense must be ordinary and necessary.

In addition, a deductible amount must be reasonable in relation to the benefit expected. For example, if you’re attempting to land a $3,000 deal, a $65 lunch with a potential client should be OK with the IRS. (Keep in mind that the Tax Cuts and Jobs Act eliminated most deductions for entertainment expenses but retained the 50% deduction for business meals.)

Examples of taxpayers who lost deductions in court

Not surprisingly, the IRS and courts don’t always agree with taxpayers about what qualifies as ordinary and necessary expenditures. Here are three 2023 cases to illustrate some of the issues:

- A married couple owned an engineering firm. For two tax years, they claimed depreciation of $76,264 on three vehicles, but didn’t provide required details including each vehicle’s ownership, cost and useful life. They claimed $34,197 in mileage deductions and provided receipts and mileage logs, but the U.S. Tax Court found they didn’t show any related business purposes. The court also found the mileage claimed included commuting costs, which can’t be written off. The court disallowed these deductions and assessed taxes and penalties. (TC Memo 2023-39)

- The Tax Court ruled that a married couple wasn’t entitled to business tax deductions because the husband’s consulting company failed to show that it was engaged in a trade or business. In fact, invoices produced by the consulting company predated its incorporation. And the court ruled that even if the expenses were legitimate, they weren’t properly substantiated. (TC Memo 2023-80)

- A physician specializing in gene therapy had multiple legal issues and deducted legal expenses of $360,295 for two years on joint Schedule C business tax returns. The Tax Court found that most of the legal fees were to defend the husband against personal conduct issues. The court denied the deduction for personal legal expenses but allowed a deduction for $13,000 for business-related legal expenses. (TC Memo 2023-42)

Proceed with caution

The deductibility of some expenses is clear. But for other expenses, it can get more complicated. Generally, if an expense seems like it’s not normal in your industry — or if it could be considered fun, personal or extravagant in nature — you should proceed with caution. And keep careful records to substantiate the expenses you’re deducting. Consult with us for guidance.

© 2023

Casualty loss tax deductions may help disaster victims in certain cases

- Details

- Published: 28 September 2023 28 September 2023

This year, many Americans have been victimized by wildfires, severe storms, flooding, tornadoes and other disasters. No matter where you live, unexpected disasters may cause damage to your home or personal property. Before the Tax Cuts and Jobs Act (TCJA), eligible casualty loss victims could claim a deduction on their tax returns. But currently, there are restrictions that make these deductions harder to take.

What’s considered a casualty for tax purposes? It’s a sudden, unexpected or unusual event, such as a hurricane, tornado, flood, earthquake, fire, act of vandalism or a terrorist attack.

Many unable to claim a tax break

For losses incurred from 2018 through 2025, the TCJA generally eliminates deductions for personal casualty losses, except for losses due to federally declared disasters.

Note: There’s an exception to the general rule of allowing casualty loss deductions only in federally declared disaster areas. If you have personal casualty gains because your insurance proceeds exceed the tax basis of the damaged or destroyed property, you can deduct personal casualty losses that aren’t due to a federally declared disaster up to the amount of your personal casualty gains.

Claim a refund with a special election

If your casualty loss is due to a federally declared disaster, a special election allows you to deduct the loss on your tax return for the preceding year and claim a refund. If you’ve already filed your return for the preceding year, you can file an amended return to make the election and claim the deduction in the earlier year. This can potentially help you get extra cash when you need it.

This election must be made no later than six months after the due date (without considering extensions) for filing your tax return for the year in which the disaster occurs. However, the election itself must be made on an original or amended return for the preceding year.

Calculating the deduction

You must take the following three steps to calculate the casualty loss deduction for personal-use property in an area declared a federal disaster:

- Subtract any insurance proceeds.

- Subtract $100 per casualty event.

- Combine the results from the first two steps and then subtract 10% of your adjusted gross income (AGI) for the year you claim the loss deduction.

Important: Another factor that makes it harder to claim a casualty loss than it was years ago is that you must itemize deductions to claim one. Through 2025, fewer people will itemize because the TCJA significantly increased the standard deduction amounts. For 2023, they’re $13,850 for single filers, $20,800 for heads of households, and $27,700 for married joint-filing couples. So even if you qualify for a casualty deduction, you might not get any tax benefit because you don’t have enough itemized deductions.

Lawmakers debate the issue

Earlier this year, a bipartisan group of lawmakers in Washington introduced a bill that would make the deduction available to more taxpayers. The proposed Casualty Loss Deduction Restoration Act would reinstate the deduction to all taxpayers with a casualty loss — not just those located in a federal disaster declaration area. Passage of the bill is uncertain at this time.

We can help

The rules described above are for personal property. Keep in mind that the rules for business or income-producing property are different and other rules may apply. (It’s easier to get a deduction for a business property casualty loss.) If you’re a victim of a disaster, we can help you understand the complex tax deduction rules.

© 2023

What are the tax implications of winning money or valuable prizes?

- Details

- Published: 26 September 2023 26 September 2023

If you gamble or buy lottery tickets and you’re lucky enough to win, congratulations! After you celebrate, be aware that there are tax consequences attached to your good fortune.

Winning at gambling

For tax purposes, it doesn’t matter if you win at the casino, a bingo hall or elsewhere. You must report 100% of your winnings as taxable income. They’re reported on an “Other income” line of your 1040 tax return. To measure your winnings on a particular wager, use the net gain. For example, if a $40 bet at the racetrack turns into a $130 win, you’ve won $90, not $130.

You must separately keep track of losses. They’re deductible, but only as itemized deductions. Therefore, if you don’t itemize and instead take the standard deduction, you can’t deduct gambling losses. In addition, gambling losses are only deductible up to the amount of gambling winnings. So you can use losses to “wipe out” gambling income but you can’t show a gambling tax loss.

Maintain good records of your losses during the year. Keep a detailed diary in which you note the date, place, amount and type of loss, as well as the name of anyone who was with you. Save all documentation, such as checks or credit slips.

Note: Different rules apply to people who qualify as professional gamblers.

Winning the lottery

Of course, the chances of winning big in the lottery are slim. But if you don’t follow the tax rules after winning, the chances of hearing from the IRS are much higher.

Lottery winnings are taxable. This is the case for cash prizes and for the fair market value of any noncash prizes, such as a car or vacation. Depending on your other income and the amount of your winnings, your federal tax rate may be as high as 37%. You may also be subject to state income tax.

You report lottery winnings as income in the year, or years, you actually receive them. In the case of noncash prizes, this would be the year the prize is received. With cash, if you take the winnings in annual installments, you only report each year’s installment as income for that year.

If you win more than $5,000 in the lottery or certain types of gambling, 24% must be withheld for federal tax purposes. You’ll receive a Form W-2G from the payer (lottery agency, casino, etc.) showing the amount paid to you and the federal tax withheld. (The payer also sends this information to the IRS.) If state tax is withheld, that amount may also be shown on Form W-2G.

Since your federal tax rate can be up to 37%, which is well above the 24% withheld, the withholding may not be enough to cover your federal tax bill. Therefore, you may have to make estimated tax payments — and you may be assessed a penalty if you fail to do so. In addition, you may be required to make state and local estimated tax payments.

We can help

If you’re fortunate enough to hit a sizable jackpot, there are other issues to consider, including estate planning. This article only covers the basic tax rules. Contact us with questions. We can help you minimize taxes and stay in compliance with all the requirements.

© 2023

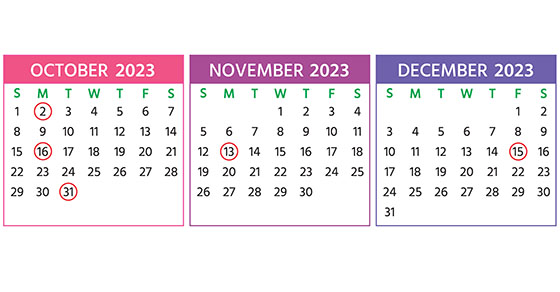

2023 Q4 tax calendar: Key deadlines for businesses and other employers

- Details

- Published: 25 September 2023 25 September 2023

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2023. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Note: Certain tax-filing and tax-payment deadlines may be postponed for taxpayers who reside in or have businesses in federally declared disaster areas.

Monday, October 2

- The last day you can initially set up a SIMPLE IRA plan, provided you (or any predecessor employer) didn’t previously maintain a SIMPLE IRA plan. If you’re a new employer that comes into existence after October 1 of the year, you can establish a SIMPLE IRA plan as soon as administratively feasible after your business comes into existence.

Monday, October 16

- If a calendar-year C corporation that filed an automatic six-month extension:

- File a 2022 income tax return (Form 1120) and pay any tax, interest and penalties due.

- Make contributions for 2022 to certain employer-sponsored retirement plans.

- Establish and contribute to a SEP for 2022, if an automatic six-month extension was filed.

Tuesday, October 31

- Report income tax withholding and FICA taxes for third quarter 2023 (Form 941) and pay any tax due. (See exception below under “November 13.”)

Monday, November 13

- Report income tax withholding and FICA taxes for third quarter 2023 (Form 941), if you deposited on time (and in full) all of the associated taxes due.

Friday, December 15

- If a calendar-year C corporation, pay the fourth installment of 2023 estimated income taxes.

Contact us if you’d like more information about the filing requirements and to ensure you’re meeting all applicable deadlines.

© 2023

Evaluate whether a Health Savings Account is beneficial to you

- Details

- Published: 22 September 2023 22 September 2023

With the escalating cost of health care, many people are looking for a more cost-effective way to pay for it. For eligible individuals, a Health Savings Account (HSA) offers a tax-favorable way to set aside funds (or have an employer do so) to meet future medical needs. Here are four tax benefits:

- Contributions made to an HSA are deductible, within limits,

- Earnings on the funds in the HSA aren’t taxed,

- Contributions your employer makes aren’t taxed to you, and

- Distributions from the HSA to cover qualified medical expenses aren’t taxed.

Eligibility

To be eligible for an HSA, you must be covered by a “high deductible health plan.” For 2023, a high deductible health plan is one with an annual deductible of at least $1,500 for self-only coverage, or at least $3,000 for family coverage. (These amounts are scheduled to increase to $1,600 and $3,200 for 2024.)

For self-only coverage, the 2023 limit on deductible contributions is $3,850. For family coverage, the 2023 limit on deductible contributions is $7,750. (These amounts are scheduled to increase to $4,150 and $8,300 for 2024.) Additionally, annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits for 2023 can’t exceed $7,500 for self-only coverage or $15,000 for family coverage ($8,050 and $16,100 for 2024).

An individual (and the individual’s covered spouse) who has reached age 55 before the close of the year (and is an eligible HSA contributor) may make additional “catch-up” contributions for 2023 and 2024 of up to $1,000 per year.

HSAs may be established by, or on behalf of, any eligible individual.

Deduction limits

You can deduct contributions to an HSA for the year up to the total of your monthly limitation for the months you were eligible. For 2023, the monthly limitation on deductible contributions for a person with self-only coverage is 1/12 of $3,850. For an individual with family coverage, the monthly limitation on deductible contributions is 1/12 of $7,750. Thus, deductible contributions aren’t limited by the amount of the annual deductible under the high deductible health plan.

Also, taxpayers who are eligible individuals on the first day of the last month of the tax year are treated as having been eligible individuals for the entire year for purposes of computing the annual HSA contribution.

However, if an individual is enrolled in Medicare, he or she is no longer eligible under the HSA rules and contributions to an HSA can no longer be made.

On a once-only basis, taxpayers can withdraw funds from an IRA and transfer them tax-free to an HSA. The amount transferred can be up to the maximum deductible HSA contribution for the type of coverage (individual or family) in effect at the transfer time. The amount transferred is excluded from gross income and isn’t subject to the 10% early withdrawal penalty.

Taking distributions

HSA distributions to cover an eligible individual’s qualified medical expenses (or those of his or her spouse or dependents, if covered) aren’t taxed. Qualified medical expenses for these purposes generally means those that would qualify for the medical expense itemized deduction. If funds are withdrawn from the HSA for other reasons, the withdrawal is taxable. Additionally, an extra 20% tax will apply to the withdrawal, unless it’s made after reaching age 65 or in the event of death or disability.

As you can see, an HSA offers a very flexible option for providing health care coverage, but the rules are somewhat complicated. Contact us if you have questions.

© 2023

It’s important to understand how taxes factor into M&A transactions

- Details

- Published: 20 September 2023 20 September 2023

In recent years, merger and acquisition activity has been strong in many industries. If your business is considering merging with or acquiring another business, it’s important to understand how the transaction will be taxed under current law.

Stocks vs. assets

From a tax standpoint, a transaction can basically be structured in two ways:

1. Stock (or ownership interest) sale. A buyer can directly purchase a seller’s ownership interest if the target business is operated as a C or S corporation, a partnership, or a limited liability company (LLC) that’s treated as a partnership for tax purposes.

The now-permanent 21% corporate federal income tax rate under the Tax Cuts and Jobs Act (TCJA) makes buying the stock of a C corporation somewhat more attractive. Reasons: The corporation will pay less tax and generate more after-tax income. Plus, any built-in gains from appreciated corporate assets will be taxed at a lower rate when they’re eventually sold.

The TCJA’s reduced individual federal tax rates may also make ownership interests in S corporations, partnerships and LLCs more attractive. Reason: The passed-through income from these entities also will be taxed at lower rates on a buyer’s personal tax return. However, the TCJA’s individual rate cuts are scheduled to expire at the end of 2025, and, depending on future changes in Washington, they could be eliminated earlier or extended.

2. Asset sale. A buyer can also purchase the assets of a business. This may happen if a buyer only wants specific assets or product lines. And it’s the only option if the target business is a sole proprietorship or a single-member LLC that’s treated as a sole proprietorship for tax purposes.

Note: In some circumstances, a corporate stock purchase can be treated as an asset purchase by making a “Section 338 election.” Ask us if this would be beneficial in your situation.

Buyer vs. seller preferences

For several reasons, buyers usually prefer to purchase assets rather than ownership interests. Generally, a buyer’s main objective is to generate enough cash flow from an acquired business to pay any acquisition debt and provide an acceptable return on the investment. Therefore, buyers are concerned about limiting exposure to undisclosed and unknown liabilities and minimizing taxes after the deal closes.

A buyer can step up (increase) the tax basis of purchased assets to reflect the purchase price. Stepped-up basis lowers taxable gains when certain assets, such as receivables and inventory, are sold or converted into cash. It also increases depreciation and amortization deductions for qualifying assets.

Meanwhile, sellers generally prefer stock sales for tax and nontax reasons. One of their main objectives is to minimize the tax bill from a sale. That can usually be achieved by selling their ownership interests in a business (corporate stock, or partnership or LLC interests) as opposed to selling business assets.

With a sale of stock or other ownership interest, liabilities generally transfer to the buyer and any gain on sale is generally treated as lower-taxed long-term capital gain (assuming the ownership interest has been held for more than one year).

Keep in mind that other areas, such as employee benefits, can also cause unexpected tax issues when merging with, or acquiring, a business.

Professional advice is critical

Buying or selling a business may be the most important transaction you make during your lifetime, so it’s important to seek professional tax advice as you negotiate. After a deal is done, it may be too late to get the best tax results. Contact us for the best way to proceed.

© 2023

Spouse-run businesses face special tax issues

- Details

- Published: 13 September 2023 13 September 2023

Do you and your spouse together operate a profitable unincorporated small business? If so, you face some challenging tax issues.

The partnership issue

An unincorporated business with your spouse is classified as a partnership for federal income tax purposes, unless you can avoid that treatment. Otherwise, you must file an annual partnership return, on Form 1065. In addition, you and your spouse must be issued separate Schedule K-1s, which allocate the partnership’s taxable income, deductions and credits between the two of you. This is only the beginning of the unwelcome tax compliance tasks.

The self-employment (SE) tax problem

The SE tax is how the government collects Social Security and Medicare taxes from self-employed individuals. For 2023, the SE tax consists of 12.4% Social Security tax on the first $160,200 of net SE income plus 2.9% Medicare tax. Once your 2023 net SE income surpasses the $160,200 ceiling, the Social Security tax component of the SE tax ends. But the 2.9% Medicare tax component continues before increasing to 3.8% — thanks to the 0.9% additional Medicare tax — if the combined net SE income of a married joint-filing couple exceeds $250,000.

With your joint Form 1040, you must include a Schedule SE to calculate SE tax on your share of the net SE income passed through to you by your spousal partnership. The return must also include a Schedule SE for your spouse to calculate the tax on your spouse’s share of net SE income passed through to him or her. This can result in a big SE tax bill.

For example, let’s say you and your spouse each have net 2023 SE income of $150,000 ($300,000 total) from your profitable 50/50 partnership business. The SE tax on your joint tax return is a whopping $45,900 ($150,000 x 15.3% x 2). That’s on top of regular federal income tax.

Here are some possible tax-saving solutions.

Strategy 1: Use an IRS-approved method to minimize SE tax in a community property state

Under IRS Revenue Procedure 2002-69, for federal tax purposes, you can treat an unincorporated spousal business in a community property state as a sole proprietorship operated by one of the spouses. By effectively allocating all the net SE income to the proprietor spouse, only the first $160,200 of net SE income is hit with the 12.4% Social Security tax. That can cut your SE tax bill.

Strategy 2: Convert a spousal partnership into an S corporation and pay modest salaries

If you and your unincorporated spousal business aren’t in a community property state, consider converting the business to S corporation status to reduce Social Security and Medicare taxes. That way, only the salaries paid to you and your spouse get hit with the Social Security and Medicare tax, collectively called FICA tax. You can then pay modest, but reasonable, salaries to you and your spouse as shareholder-employees while paying out most or all remaining corporate cash flow to yourselves as FICA-tax-free cash distributions.

Strategy 3: Disband your partnership and hire your spouse as an employee

You can disband the existing spousal partnership and start running the operation as a sole proprietorship operated by one spouse. Then hire the other spouse as an employee of the proprietorship. Pay that spouse a modest cash salary. You must withhold 7.65% from the salary to cover the employee-spouse’s share of the Social Security and Medicare taxes. The proprietorship must also pay 7.65% as the employer’s half of the taxes. However, since the employee-spouse’s salary is modest, the FICA tax will also be modest.

With this strategy, you file only one Schedule SE — for the spouse treated as the proprietor — with your joint tax return. That minimizes the SE tax, because no more than $160,200 (for 2023) is exposed to the 12.4% Social Security portion of the SE tax.

Find tax-saving strategies

Having a profitable unincorporated business with your spouse that’s classified as a partnership for federal income tax purposes can lead to compliance headaches and high SE tax bills. Work with us to identify appropriate tax-saving strategies.

© 2023

Plan now for year-end gifts with the gift tax annual exclusion

- Details

- Published: 07 September 2023 07 September 2023

Now that Labor Day has passed, the holidays are just around the corner. Many people may want to make gifts of cash or stock to their loved ones. By properly using the annual exclusion, gifts to family members and loved ones can reduce the size of your taxable estate, within generous limits, without triggering any estate or gift tax. The exclusion amount for 2023 is $17,000.

The exclusion covers gifts you make to each recipient each year. Therefore, a taxpayer with three children can transfer $51,000 to the children this year free of federal gift taxes. If the only gifts made during a year are excluded in this fashion, there’s no need to file a federal gift tax return. If annual gifts exceed $17,000, the exclusion covers the first $17,000 per recipient, and only the excess is taxable. In addition, even taxable gifts may result in no gift tax liability thanks to the unified credit (discussed below).

Note: This discussion isn’t relevant to gifts made to a spouse because these gifts are free of gift tax under separate marital deduction rules.

Married taxpayers can split gifts

If you’re married, a gift made during a year can be treated as split between you and your spouse, even if the cash or gift property is actually given by only one of you. Thus, by gift-splitting, up to $34,000 a year can be transferred to each recipient by a married couple because of their two annual exclusions. For example, a married couple with three married children can transfer a total of $204,000 each year to their children and to the children’s spouses ($34,000 for each of six recipients).

If gift-splitting is involved, both spouses must consent to it. Consent should be indicated on the gift tax return (or returns) that the spouses file. The IRS prefers that both spouses indicate their consent on each return filed. Because more than $17,000 is being transferred by a spouse, a gift tax return (or returns) will have to be filed, even if the $34,000 exclusion covers total gifts. We can prepare a gift tax return (or returns) for you, if more than $17,000 is being given to a single individual in any year.

“Unified” credit for taxable gifts

Even gifts that aren’t covered by the exclusion, and are thus taxable, may not result in a tax liability. This is because a tax credit wipes out the federal gift tax liability on the first taxable gifts that you make in your lifetime, up to $12.92 million for 2023. However, to the extent you use this credit against a gift tax liability, it reduces (or eliminates) the credit available for use against the federal estate tax at your death.

Be aware that gifts made directly to a financial institution to pay for tuition or to a health care provider to pay for medical expenses on behalf of someone else don’t count towards the exclusion. For example, you can pay $20,000 to your grandson’s college for his tuition this year, plus still give him up to $17,000 as a gift.

Annual gifts help reduce the taxable value of your estate. The estate and gift tax exemption amount is scheduled to be cut drastically in 2026 to the 2017 level when the related Tax Cuts and Jobs Act provisions expire (unless Congress acts to extend them). Making large tax-free gifts may be one way to recognize and address this potential threat. They could help insulate you against any later reduction in the unified federal estate and gift tax exemption.

© 2023